Late last year in an initial discovery meeting with a couple of amazing new clients, when I asked them what was the one key piece of value they’d like from us in developing a financial strategy for them, they beautifully articulated what most clients essentially want…“We want to have the right balance between Lifestyle vs Legacy”.

The uncomplicated power of this has stayed with me. Of course lifestyle and legacy mean different things to different people. In this case is was to essentially “Cover our lifestyle now. Cover our lifestyle later. And pass on a decent amount of assets to our kids to carry the torch”.

Up until now this Wealth Creation for Generation X blog has been largely focused on providing you with valuable and tangible ideas & strategies to enable you to create future financial freedom. To cover your Desired “Retirement” Spending for life after work…ideally all the way through at least age 90+. But what if you are just as keen to leave a Legacy for your children than you are to build towards creating your own financial freedom? If you are already starting from a strong financial base and/or you are excited about creating Generational Wealth…then this blog is aimed at you.

You may have already read Wealth Creation for Generation X – How much is enough…really? If you haven’t, to briefly recap…

You may remember that I’m not a big believer in the whole concept of retirement. Why not work well into your 70’s and beyond for the purpose, contribution, personal growth & social interaction? But, regardless if this excites you or not, at least aim to reach the point where you have built enough wealth that you don’t have to work for the money any more. It’s about having freedom to choose. Creating Financial Freedom is the aim of the game…not retirement.

Before you build enough assets to create Generational Wealth, you first have to build enough assets to create your own Financial Freedom….to have enough investment assets to cover your own Desired “Retirement” Spending well beyond current life expectancy. Because as covered in Wealth Creation for Gen X – Is Superannuation still so super? Gen X Life Expectancy is likely to increase dramatically with medical & technological advances.

Recapping on how much is enough to create your own Financial Freedom, let’s say you are currently 40 years of age and you and your partner would like to achieve Financial Freedom by age 60 and have the ability to spend $100,000 per year (in today’s dollars) all the way through to age 90. You’ll need around $1,750,000 in investment assets at age 60 to fund this level of lifestyle. However this is in today’s terms. Assuming inflation of 3%, at age 60 you will actually need around 1.8 x $1,750,000 or approx. $3,150,000 in future dollars – investing in a Balanced mix of assets. (You can refer to Wealth Creation for Generation X – How much is enough…really? to see the mix of assets required outside of Superannuation to still be Financially Free by age 60…even if the rules change like I think they will and you can’t access you Super until age 70).

So if you are around age 40 (like me this year) then you’ll need at least around $3,150,000+ in total future investment assets (excluding your home or other lifestyle assets) at age 60 (or age 65 if you are currently around age 45) if you want to be in a position to cover a Desired Retired Spending level of around $100,000 in today’s terms, all the way through to your 90’s. But very importantly…this assumes that in the end the only assets you have left is the value of the family home. However chances are by then this asset could be long gone to help fund future age care or other medical costs. Therefore it’s not a given that the value of the family home will be there to pass on to the next generation.

Taking all this into account, if you would not only like to build enough assets to create Future Financial Freedom for yourself but also create Generational Wealth by not needing draw down / reduce your capital base beyond “Retirement”, then How much is enough…really?

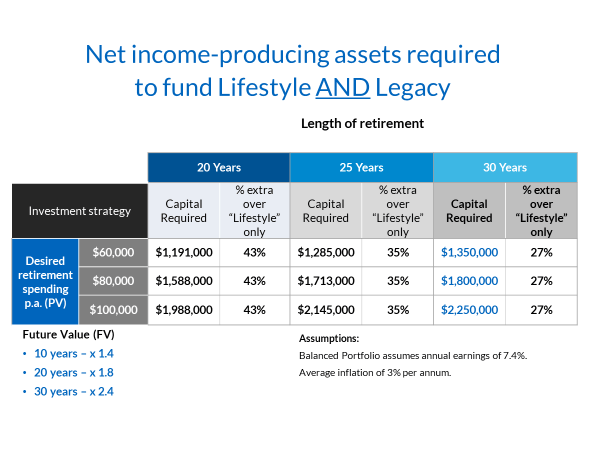

Whilst is not always about the numbers, in this case it kind of is. See below for the summary of what is required. The table below shows what level of net investment assets (superannuation, investment property equity, shares and cash etc) is required to cover not only your own financial freedom level lifestyle spending but also pass on a financial legacy after 20, 25 or 30 years to the next generation/s equivalent to the same amount (present value) as what you had in the year you choose to stop work. In other words what level of assets is required to cover your own Future Financial Freedom but also maintain the buying power of the capital to build Generational Wealth? This analysis also looks at what extra investment assets are required (in % terms) over and above the amount required to achieve financial freedom and fund your “desired future lifestyle”.

As above, taking a “Desired Retirement Spending” of $100,000 over 30 years as an example, if this was your goal, going by How much is enough…really? as a guide, you’d need around $1,750,000 of investment assets to fund your lifestyle from say age 60 through to age 90 in an ongoing manner. If however you wanted to take it to the next level and cover your “desired retirement spending” and at the 30 year mark pass on the present value equivalent of $1,750,000, based on the above table, you’d need around $2,250,000 (in today’s terms) in investment assets assets at the year you’d like to be in a position to chose to stop work. In other words $1,750,000 would be working hard for you to cover your own financial freedom, and $500,000 would be working hard for you to maintain the buying power of this and build Generational Wealth. This is around 27% extra Investment assets required over and above the level to achieve your own future financial freedom for 30 years (Out of interest the shorter the “Length of Retirement” the greater level of assets required, in % terms, as you have less years of compound growth to be building Generational Wealth).

Importantly like before though this amount required of $2,250,000 is in today’s terms. If you are currently around 20 years away from wanting to choose to stop work and be financially free with the ability to cover a lifestyle of say $100,000 in today’s terms, then in 20 years time you will actually need around 1.8 x $2,250,000 or approx. $4,050,000 in future dollar value – investing in a Balanced mix of assets.

It’s been said that “A person who doesn’t read is no better off than a person who cannot read”…along these lines I believe that in many ways “A person who has the means & income to build financial freedom & generational wealth…and doesn’t, is no better off than a person who doesn’t have the means & income to build wealth”.

If you are on track to covering your own financial freedom, why not take it that next step further and build Generational Wealth? As above, stretched over a 20 year game plan, it actually doesn’t take that much more on top of the level of assets required to create Future Financial Freedom. I know an extra $900,000 (in future terms) over 20 years sounds like a fair bit more than “not much more”. But it might just come down to pushing yourself to find the extra cash flow to make it happen. See Wealth Creation for Generation X – Making yourself more Valuable for a few ideas. It might take contributing a bit extra into super, increase your regular investment plan, buying an (additional) investment property or accelerating the debt reduction on an existing investment property (or a combination of a several strategies). Maybe it’s a matter of working for 3-5 more years to delay drawing on capital and allowing for the power of compound growth. Either way it will take some sacrifices, some trades offs, and mapping out a proper Game Plan.

I don’t know about you, but I really like the idea of our future grand kids & great grand kids having a strong financial base (rather than starting from scratch each generation) and not only be motivated to carry the torch for their future generations, but more importantly to do good things and make a meaningful impact on the world with the assets passed on from the generations before them.

If you like the concept of creating Future Financial Freedom and Generational Wealth, it’s time to take it to the next level and start creating your own ideal financial future.

Matthew Morrison is the Director of Wealth Advisory at The Practice, a Personal Wealth Advisory & Business Advisory firm based in Melbourne & Sydney. Matt along with The Practice team are committed to and passionate about developing & implementing wealth creation strategies for clients to enable them to Fuel their Family’s Future (while protecting them along the journey).

Matt and The Practice team can be contacted via http://thepractice.com.au or (03) 8888 4000.

Disclaimer – the above views and ideas are general advice only and are purely the opinions of the author. It’s important that you seek professional advice tailored to your needs before taking action regarding your financial future. (Also, unfortunately we can’t guarantee the top quality content in this blog will secure you a prosperous future if you ‘try this at home’, or trust any old backyard financial adviser to help you & your family with what is one of the most important decisions you’ll ever make…who to partner with on your quest to build wealth & create future Financial Freedom).