On the back of the theme of last week on the importance of clarity and the idea of “begin with the end in mind”, this week lets explore “How much is enough?”…or more specifically “How much is enough for Generation X?”

For the record I’m not a big believer in the whole concept of retirement. Many Generation Xers see the idea of future retirement as an unproductive and inactive time…and this doesn’t appeal to them at all. A number of people these days plan to never retire. And if this is you then hats off to you. By all means keep working for the purpose, contribution and social interaction…but at least aim to reach the point where you have built enough wealth that you don’t have to work for the money any more. It’s about having freedom to choose. Creating Financial Freedom is the aim of the game…not retirement.

But how much is enough?…well it depends. It depends on your future lifestyle goals…and it depends on who you ask.

The latest report released by ASFA (The Association of Superannuation Funds of Australia) indicates that the annual spending required for a couple to live a “comfortable” lifestyle in retirement is $59,160. They estimate that the superannuation/investment assets required to fund this is around $640,000 (earning a Balanced rate of return). Whilst well-meaning and no doubt a good guide for Baby Boomers looking to retire in the coming years…for those of you who are members of Generation X (currently aged 35-50) this can provide a false sense of security. Here’s why;

- Firstly, the numbers assume a life expectancy in retirement of 20 years…age 85 (assuming retirement is age 65). With medical advances there is every chance that a fair proportion of Generation X will live past 100. Without proper planning, Generation X run the very real risk of out-living their money.

- Secondly, it assumes that the Age Pension is available to assist in funding the retirees cost of living. If you are 45 years of age or under…I’ll go out on a limb and say that the Age Pension will not be around by the time you retire. If it is, then it may only be available when you are down to your last dollar and have been forced to sell your house!

- Thirdly, I’m not sure that $59,160 will really cover a comfortable “retirement” when you factor in the travel you will ideally want to do, along with potentially helping your kids in some meaningful way. Most clients I work with would want the ability to spend $80,000-$100,000 per annum (in today’s dollars) for life after work – including around $20,000+ per year in travel. And be able to do this ideally right throughout their “retirement” years, not just for 6 or 7 years and then go back to relying on the government Age Pension (or their kids).

Additionally, as flagged in a previous post, right now Generation X can access their superannuation at age 60. However, if you are like me and in the younger half of Generation X (say around age 42 or under) then, in my humble opinion, you will not be able to access your superannuation until age 70 – at least that’s what I think you should be mentally preparing for. It’s crucial for Generation Xers to build wealth outside of superannuation in tandem with building wealth inside of superannuation.

Without getting overly complicated…so how much is actually enough? (I hear you say).

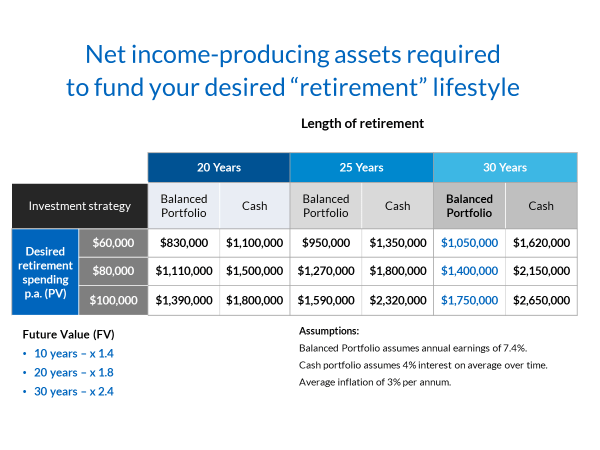

The below table looks at the level of total investment assets (excluding your home) needed to fund various Desired Retirement Spending levels (this assumes zero Age Pension and zero financial assistance from anyone but yourself).

Take the example where to create Financial Freedom you are aiming to be able to spend $100,000 per annum (in today’s terms) in “retirement”…and why not aim for that. If your ‘Length of Retirement’ was 30 years and if you were happy to allocate your investments in a Balanced mix of assets, then you would need around $1,750,000 (in today’s terms) in total investment assets (superannuation, investment property equity, shares, cash etc). This assumes you have zero assets left at the end apart from your home. (Incidentally, as per the table, if you took the view that you’ll put everything in cash at retirement earning an optimistic 4% then you will actually need around $2,650,000 in total investment assets (in today’s terms) as your money is not working very hard for you – One of the biggest risks you can take is not to take on any risk).

But crucially this is all “today’s dollars”, not actually what you’ll need in “future dollars” (Future Value) by the time you get there.

Let’s say you are currently 40 years of age and you and your partner would like to achieve Financial Freedom by age 60 and have the ability to spend $100,000 per year (in today’s dollars) all the way through to age 90. Then (assuming inflation of 3%) at age 60 you will actually need around 1.8 x $1,750,000 or approx. $3,150,000 in future dollars – investing in a Balanced mix of assets. (You can do the maths on the other options below if your goals or circumstances are any different). But what if you aim to achieve Financial Freedom by age 60…but can’t access your superannuation until age 70? If all your money is in superannuation, then you’ve got a bit of an issue…and you face the very real prospect of having to work for 10 years longer than you were planning.

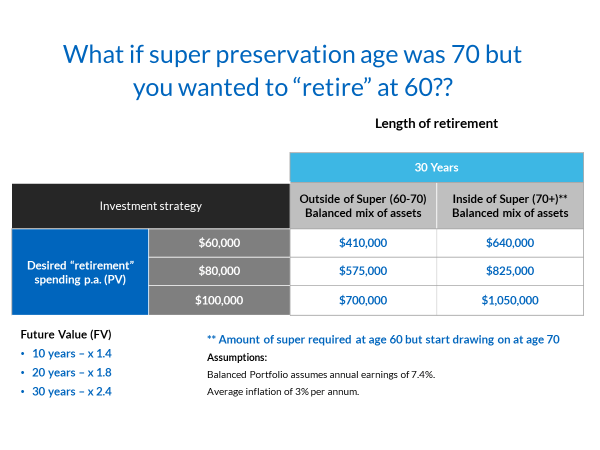

But what if you aim to achieve Financial Freedom by age 60…but can’t access your superannuation until age 70? If all your money is in superannuation, then you’ve got a bit of an issue…and you face the very real prospect of having to work for 10 years longer than you were planning.

Building part of your wealth outside of superannuation is a must!

Let’s assume again that you and your partner are a 40 year old couple looking to create Financial Freedom by age 60 with the ability to spend $100,000 per annum (in today’s dollars) ongoing. As per the table below, by age 60 you would need around $700,000 investment assets outside of superannuation with a further $1,050,000 inside of super. This is again in “today’s dollars” and (assuming inflation of 3%) at age 60 you will need around 1.8 times these amounts – approx. $1,260,000 outside of super (in future dollars) to fund your cost of living from age 60 to age 70 and approx. $1,890,000 inside of super (in future dollars at age 60) to fund your cost of living from age 70 through to around age 90…..(not quite cracking a century – but I think most of us would be content with reaching our 90’s).

For Generation Xers looking to build towards Financial Freedom, the idea “If it’s to be, it’s up to me” has never been more relevant. The government will not be in a position to help you like they are helping current Age Pensioners.

For Generation Xers looking to build towards Financial Freedom, the idea “If it’s to be, it’s up to me” has never been more relevant. The government will not be in a position to help you like they are helping current Age Pensioners.

It’s time to get moving…and start creating your own financial future.

Matthew Morrison is the Director of Wealth Advisory at The Practice, a Personal Wealth & Business Advisory firm based in Parkville, Melbourne. Matt along with The Practice team are committed to and passionate about developing and implementing financial strategies for clients to enable them to Fuel their Family’s Future.

Matt and The Practice team can be contacted via http://thepractice.com.au or (03) 8888 4000.

Pingback: Wealth Creation for Generation X – Where should you invest your money? | Wealth Creation for Generation X

Pingback: Wealth Creation for Gen X – Is Superannuation still so super? | Wealth Creation for Generation X

Pingback: Wealth Creation for Generation X – Making yourself more Valuable | Wealth Creation for Generation X

Pingback: Wealth Creation for Gen X – Why most people don’t (and won’t) achieve Financial Freedom | Wealth Creation for Generation X

Pingback: Wealth Creation for Gen X – Lifestyle vs Legacy | Wealth Creation for Generation X

Pingback: MAKING YOURSELF MORE VALUABLE - The Practice