Last week in Wealth Creation for Generation X – The Power of a Regular Investment Plan we covered the reasons a Regular Investment Plan should form part of every Gen Xer’s strategy towards future financial freedom. However, not only is a regular investment plan an effective way to build an additional income stream for life after work, it’s also a powerful way that many clients use to help fund future private secondary school costs for their young children.

Many people like the idea of being able to send their children to a private secondary school. However the cost of at least $25,000 per annum, per child from year 7-12 is substantial for one child, let alone two or more. Added to this that the $25,000 is an after tax cost, means the parents need to earn $40,000 – $50,000 pre tax (depending on their tax rate), just to pay one years school fees. Let’s say you have two children that are two years apart. The 4 years that both the kids are in secondary school together would put extreme financial stress on most couples…there may not be too many family holidays in those years. What about cash to fund your wealth creation strategy?…unlikely.

A better alternative in my opinion is to use the power of a regular investment plan and spread the education expense over a number of years and let the power of compounding pay for a good chunk of your kids education.

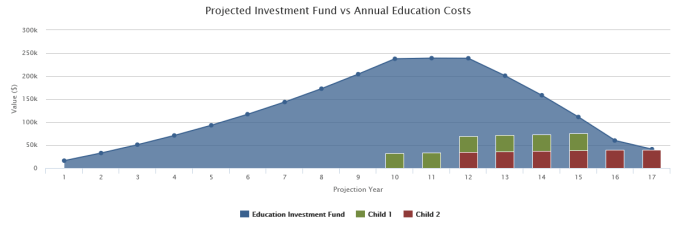

The example below assumes a couple have a 3 year old and a 1 year old and plan to send their kids to private secondary school costing $25,000 per annum (in today’s terms) from year 7-12. Assuming a Balanced mix of assets earning on average around 7.4% (the average 30 year Balanced return) and kicking it off with $2,000 initial investment, the regular investment required to fully fund their kids education would be approx $1,200 per month (indexed yearly by CPI) starting now all the way through to when the youngest child finishes year 12…still a significant commitment I know, but far less of a burden during high school years. This frees up cash flow during this time for things like family holidays…or allowing the parents to continue their wealth creation plans to build financial freedom for life after work. In this example the total education costs are $434,800. But “only” $306,400 is funded through the couples monthly investment contributions (spread over 17 years) with the other $128,400 funded by investment earnings and compound growth.

Once again with the “why shouldn’t I just pay off my mortgage” debate…if the above couple instead put $1,200 per month extra off their mortgage, all things being equal, they would then be borrowing to fund their kids education costs, and funding the full amount of $434,800, losing out on the power of compounding and creating a significant expense in mortgage repayments which would eat up cash flow and create a financial burden for many years to come.

If you have young kids, whilst establishing a regular investment account is powerful way to fund their future education costs…ideally it is only a “plan B”. Wouldn’t it be great to find a way to fund your kids education costs from future cash flow and still have this “bucket of money” available to fund your future wealth creation plans and/or provide your kids with a good start in their financial lives?

For most clients who use a regular investment plan to fund their kids future secondary school education, we actually recommend to set up two regular investment accounts 1) for their own future financial freedom, and 2) for their kids education costs (assuming this gets spent entirely by the time the youngest finishes year 12). This way each “bucket” of money is quarantined from the other and it’s clearly identifiable what the purpose is for each investment. This ensures any regular investment for yourself under #1 above is available to help fund your long term financial freedom plans and not be dramatically reduced…or wiped out, by being needed to fund the kids education.

Each to their own on Private vs Public secondary school. Who knows whether it really makes a difference. But if you have young kids that you’ll like to at least have the option of sending to private secondary school…then commencing a regular investment plan to help fund this expense is one of the smartest things you can do. Use the power of compounding and dollar cost averaging to build an “isolated bucket of money” to draw from in the future. But don’t delay getting started. The longer you wait, the less years you have to stretch the total savings over…and the less you’ll benefit from compound growth.

In a perfect world these funds won’t be required, and can instead be used for your own wealth strategy or provide the kids a strong start in the financial lives. Whether the education funding Regular Investment Plan covers all or part of the kids private school fees, or simply is a “plan B” back up…it’s far better to have the funds there than not. It’s good to have options. As the greater your financial options….the greater your financial freedom.

Matthew Morrison is the Director of Wealth Advisory at The Practice, a Personal Wealth Advisory & Business Advisory firm based in Parkville, Melbourne. Matt along with The Practice team are committed to and passionate about developing & implementing wealth creation strategies for clients to enable them to Fuel their Family’s Future (while protecting them along the journey).

Matt and The Practice team can be contacted via http://thepractice.com.au or (03) 8888 4000.

Disclaimer – the above views are general advice only and are purely the opinions of the author. It’s important that you seek professional advice tailored to your needs before taking action regarding your financial future.

I think using regular investments is an effective way to fund education expenses.

LikeLike