It’s been said that “What you do on a regular basis matters far more than what you might do every once in a while”. Of course this is true in many areas of life – exercise, relationship building, working on your golf handicap – but it’s also very much applicable to your financial strategy.

In my last blog of 2016 Wealth Creation for Gen X – Where should you invest your money? we covered the 5 main areas Gen Xer’s & Gen Y’s should focus on over time in order to build towards future financial freedom. In this week’s blog we’ll explore the most under valued and under utilised element of those 5 key wealth creation pillars…and that’s the power of a Regular Investment Plan.

At this time of year many people set a goal to have a good year financially and start investing (or invest more than they did last year). Many people may decide to invest their expected future bonus or tax return. Unfortunately in most cases this doesn’t work. Firstly, especially in relation to wanting to invest an expected tax return – most people over spend in the lead up to receiving an expected future lump sum of money (like a tax return) and by the time the funds are received, this money is usually spent already on credit cards…and the tax return is used simply to clear the credit card and get back to square. Then the person promises themselves they’ll do things differently next year…until the next shiny new toy grabs their interest. The benefit of investing a set amount of money on a regular basis rather than try to invest a yearly lump sum is that 1) it creates good habits of “paying yourself first” and spending less than you earn, and 2) you’re able to reduce risk by taking advantage of “dollar cost averaging”.

You’ve no doubt heard of dollar cost averaging before, but briefly this means you are able to manage risk better by making smaller/regular contributions over the years and even-out your investment entry price over time…compared to one yearly lump sum. When investment markets are lower, you get more for your money. When investment markets are higher, you get less for your money. Either way it avoids the risk of making that yearly lump sum which could be at a peak point in the investment/share market and at high risk of being smacked by a short term correction.

As outlined in Wealth Creation for Gen X – Good Debt versus Bad Debt I think it’s crucial to be building wealth and reducing debt in tandem with one another. The immediate question that pops into your head when I suggest you commence a regular investment for the long term may be “why shouldn’t I just pay the money off my mortgage?”. The challenge with this is that you need to live somewhere and your home won’t produce you an income in the future. Holding an investment account with the main purpose of adding to it for future wealth creation purposes, whilst using other cash flow to reduce debt…feels good mentally. The investment account becomes an “isolated bucket of money” that develops a momentum of it’s own. After you’ve been doing this for a few years the earnings from the investment can start exceeding what is being contributed. That’s when the power of this strategy really starts to take hold – by using what Einstein called “the 8th wonder of the world” – Compound Growth – and have your money work hard for you and your long term financial future.

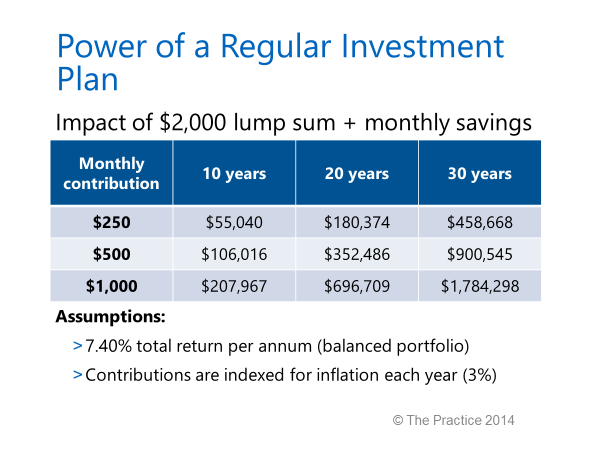

As in the table below, implementing a regular investment plan where you “take money off yourself” and pay yourself first can be a powerful way to build another income stream for the future. It shouldn’t be relied upon as your only wealth creation strategy…however it shouldn’t be ignored either. Even $500 per month invested in a Balanced mix of assets is likely to grow to a significant amount over a 20-30 year period. This is especially powerful as this money may have just been spent otherwise (remember if it’s not there you can’t spend it). This provides options and takes away the sole reliance that most people have on superannuation in order to fund your future financial freedom.

Everyone would love to see their investment accounts always making good returns….however that’s not reality. We all know that growth assets (shares and property investments) go through periods of high volatility and even negative returns. That’s why the “3 bucket concept of asset allocation” covered in previous blogs comes into play. An investment account should be part of the long term bucket of money and you should take a 7 year+ view…ideally 20+ years if you want to create substantial wealth (the time will go by anyway, you may as well make the most of it). It’s actually the regular investments made when things are low that will end up growing the most and earning you the most over time. However when short term returns are low, unfortunately that’s precisely the time that many people lose faith in a regular investment plan and start to think of withdrawing the money and allocating to cash or their mortgage. From seeing a few hundred clients carry out this strategy over the years, it’s the people that stick with it during good times and bad that end up doing the best financially by allowing both time and compound growth to work in their favour.

Everyone would love to see their investment accounts always making good returns….however that’s not reality. We all know that growth assets (shares and property investments) go through periods of high volatility and even negative returns. That’s why the “3 bucket concept of asset allocation” covered in previous blogs comes into play. An investment account should be part of the long term bucket of money and you should take a 7 year+ view…ideally 20+ years if you want to create substantial wealth (the time will go by anyway, you may as well make the most of it). It’s actually the regular investments made when things are low that will end up growing the most and earning you the most over time. However when short term returns are low, unfortunately that’s precisely the time that many people lose faith in a regular investment plan and start to think of withdrawing the money and allocating to cash or their mortgage. From seeing a few hundred clients carry out this strategy over the years, it’s the people that stick with it during good times and bad that end up doing the best financially by allowing both time and compound growth to work in their favour.

“Stick with it, when you’re hardest hit. It’s when seem worst that you must not quit” (Poem – Don’t Quit by Edgar A. Guest).

Quickly recapping on my the last blog, I like to call a regular investment plan your “pre-retirement superannuation”. What if you are currently 40 and would like to be in a position to choose to stop work at say age 60-65 and cover your desired cost of living? But what if you couldn’t access your superannuation until you are 70? Even if you had an investment property, it’s pretty hard to sell a kitchen, lounge room or half a house to free up some cash. You’d need to sell the whole thing and lose this income stream. A liquid investment account built up over the years via a regular investment plan, provides a liquid bucket of money to draw on for life after work. This delays any need to sell the investment property and hopefully sees you through to being able to access your superannuation…delaying once again the need to sell the investment property – allowing this to continue to grow and compound over time.

As with most financial goals that are made at the start of the year, “life” can have a habit of getting in the way not too long after the glow of the Christmas holiday becomes a fading memory. For this reason with a regular investment plan it’s crucial that you set yourself up for success and automate the process. This only works if you don’t have to think about it. The monthly contribution should be structured by direct debit or automated BPay payment from your internet banking, ideally scheduled for the day after you get paid to “take money off yourself” before you can think of an excuse not to invest money for the month. There will always be bills to pay…pay this like your mortgage or your rent.

You might be thinking “this is great but what do I invest my money in?”. There are a few investment structures that work well for a regular investment plan. In future blogs I’ll cover some specifics on how to go about doing this and what to invest in. Additionally in my next blog I’ll cover how many clients with young kids use the Power of a Regular Investment Plan to build funds to fully cover their children’s future private secondary school education.

For now though decide that 2017 is going to be your best financial year ever (up until this point at least) and resolve to start the habit of “paying your self first” and automating the process. If you are already investing for your future via a Regular Investment Plan, then I’d encourage you to push yourself and strive to invest/save more than you did last year.

Matthew Morrison is the Director of Wealth Advisory at The Practice, a Personal Wealth Advisory & Business Advisory firm based in Parkville, Melbourne. Matt along with The Practice team are committed to and passionate about developing & implementing wealth creation strategies for clients to enable them to Fuel their Family’s Future (while protecting them along the journey).

Matt and The Practice team can be contacted via http://thepractice.com.au or (03) 8888 4000.

Disclaimer – the above views are general advice only and are purely the opinions of the author. It’s important that you seek professional advice tailored to your needs before taking action regarding your financial future.

Pingback: Wealth Creation for Generation X – How to best fund your kids future education | Wealth Creation for Generation X

Pingback: Wealth Creation for Generation X – Structures for Regular Investment Plans | Wealth Creation for Generation X

Pingback: Wealth Creation for Generation X – Making yourself more Valuable | Wealth Creation for Generation X

Pingback: MAKING YOURSELF MORE VALUABLE - The Practice